Australia advertising landscape: 8 key facts and trends

Australians see more ads per person than most G7 countries, yet lead the world in blocking them—revealing a critical tension shaping the future of digital marketing.

This post was written in 2019. Some details may have changed since then.

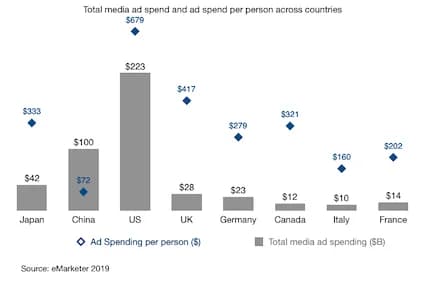

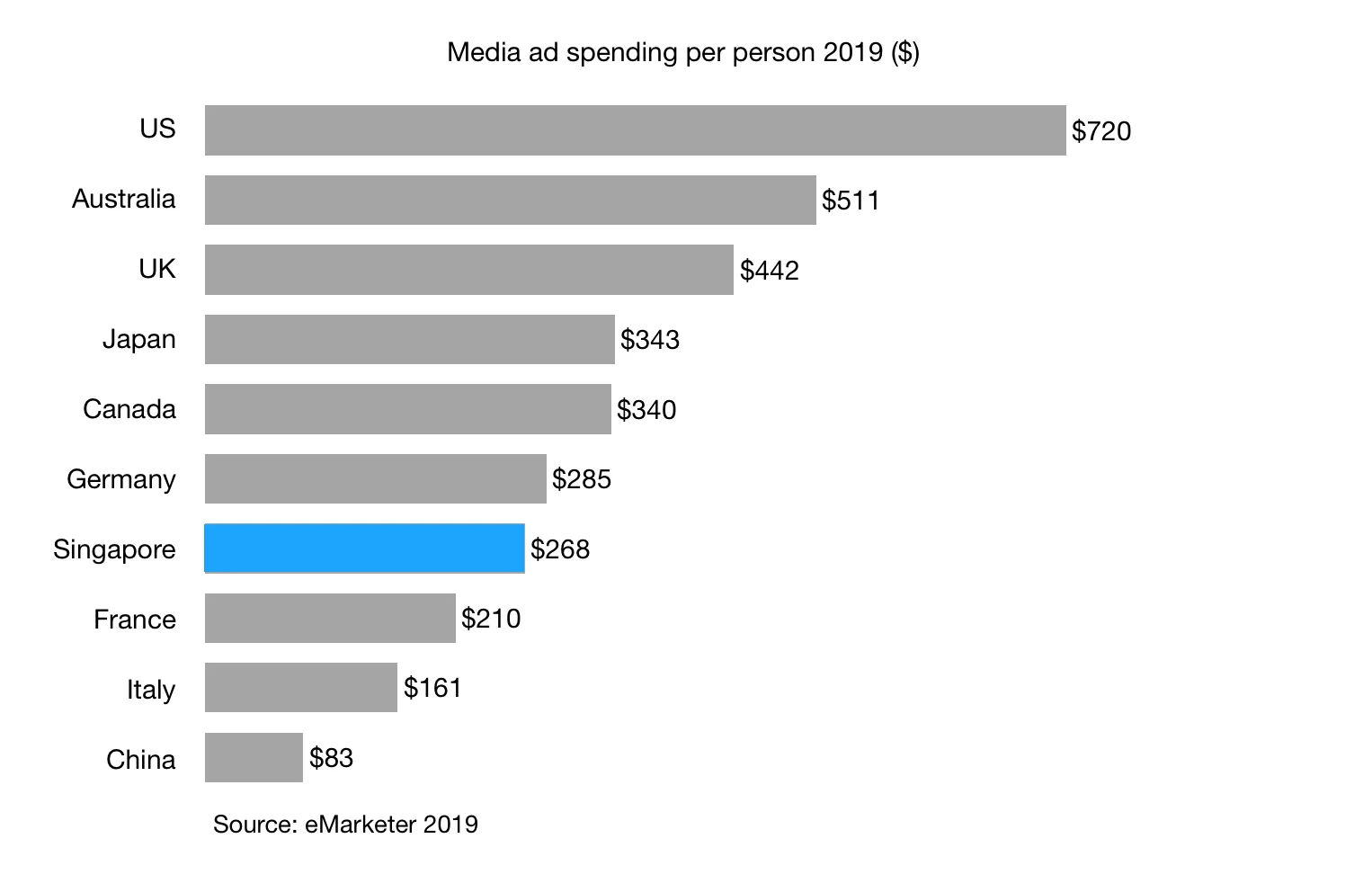

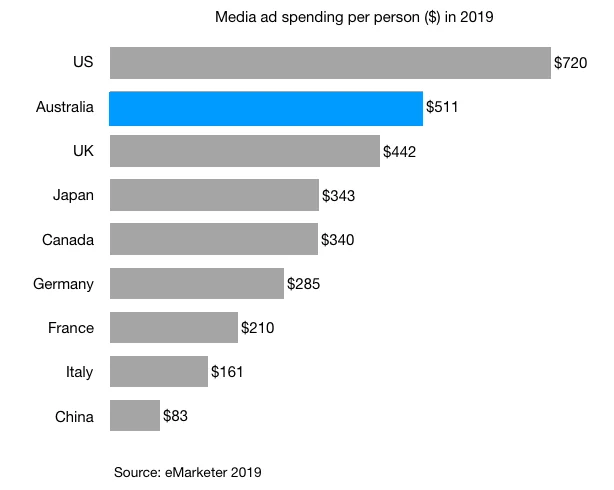

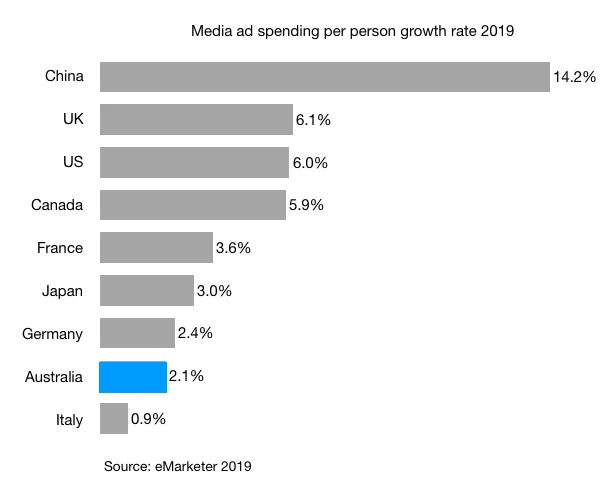

1. Media ad spending per person in Australia is higher than most G7 countries and China

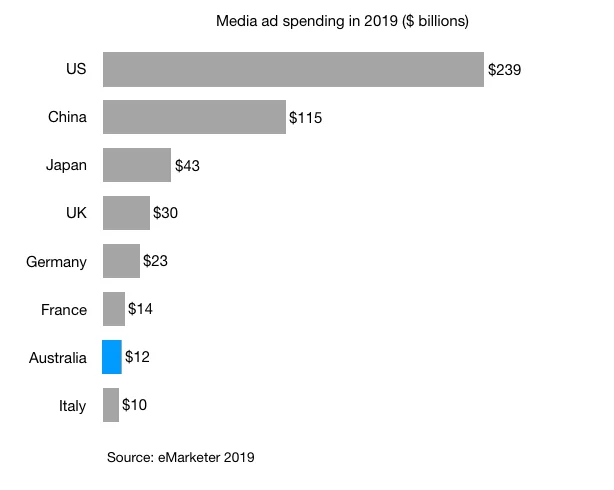

Given the size of the Australia population, it is not a surprise that their total media ad spending is tiny in comparison to other G7 countries and China.

Given the high base, it is not surprising that Australia total ad spending per person growth is expected to be flat in the next few years.

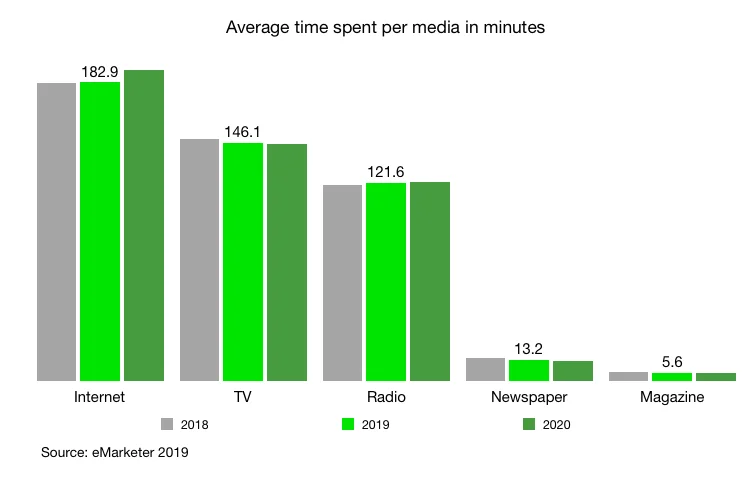

2. Australian consumers spend a roughly equal amount of time on TV and the internet

It is interesting to note that Radio remains stable over the past six years and continue to play a significant role in how Australian consumers spend their time with Media.

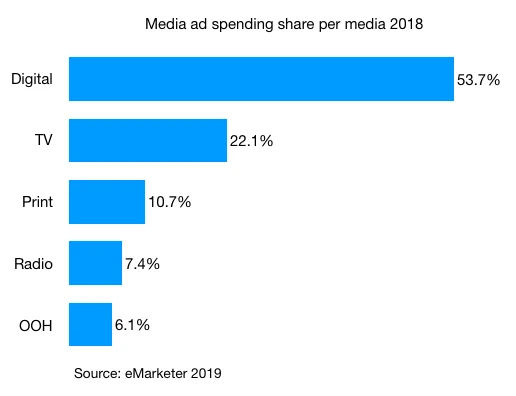

3. Given the time spent per media, digital has an outsized share of the total ad spending, while Radio has a smaller share

TV perhaps should command a proportionately more significant share of the total ad spending?

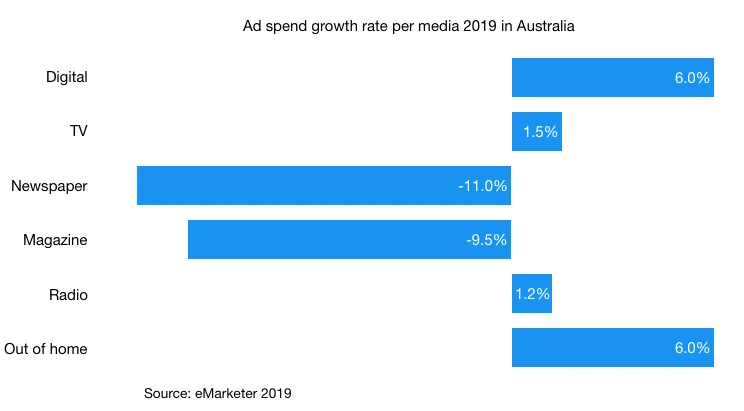

4. Over the next 3-5 years, most of the growth is coming from Digital and Out of Home, with print ad declining quickly

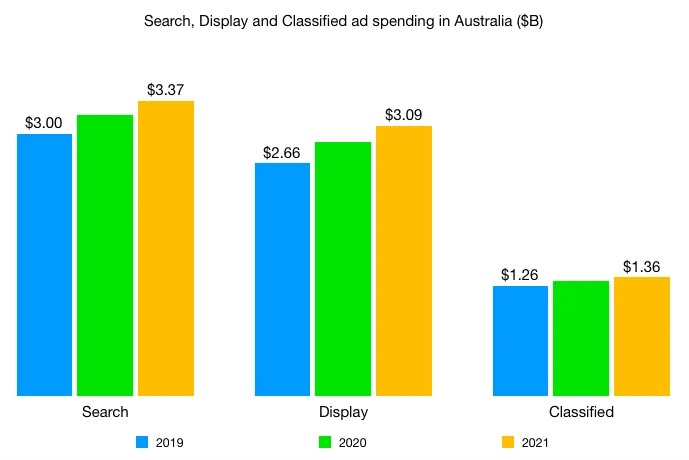

5. Within Digital, Search continues to edge display ad spend out in the next few years

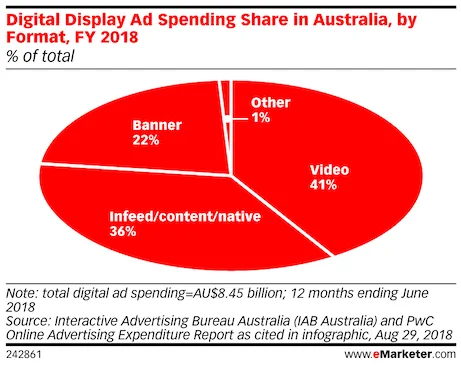

6. Within Digital display, it is not surprising that video format takes the largest share (41%)

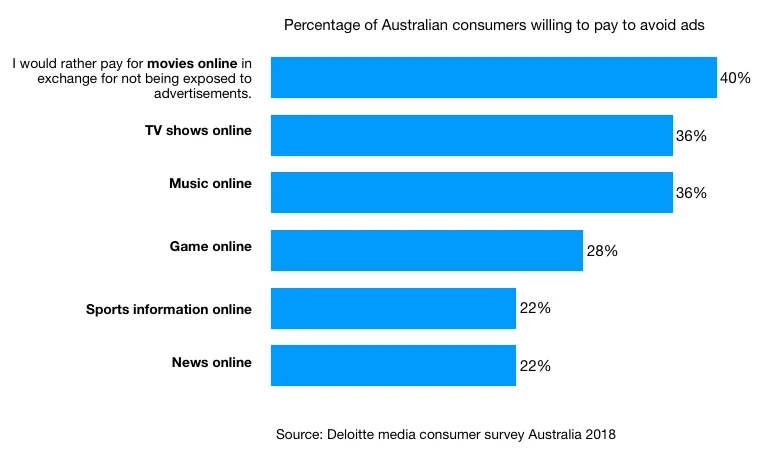

7. Depending on content type, a sizeable percentage of the Australia consumers are willing to pay for content to avoid ads

Deloitte Media consumer survey Australia 2018.

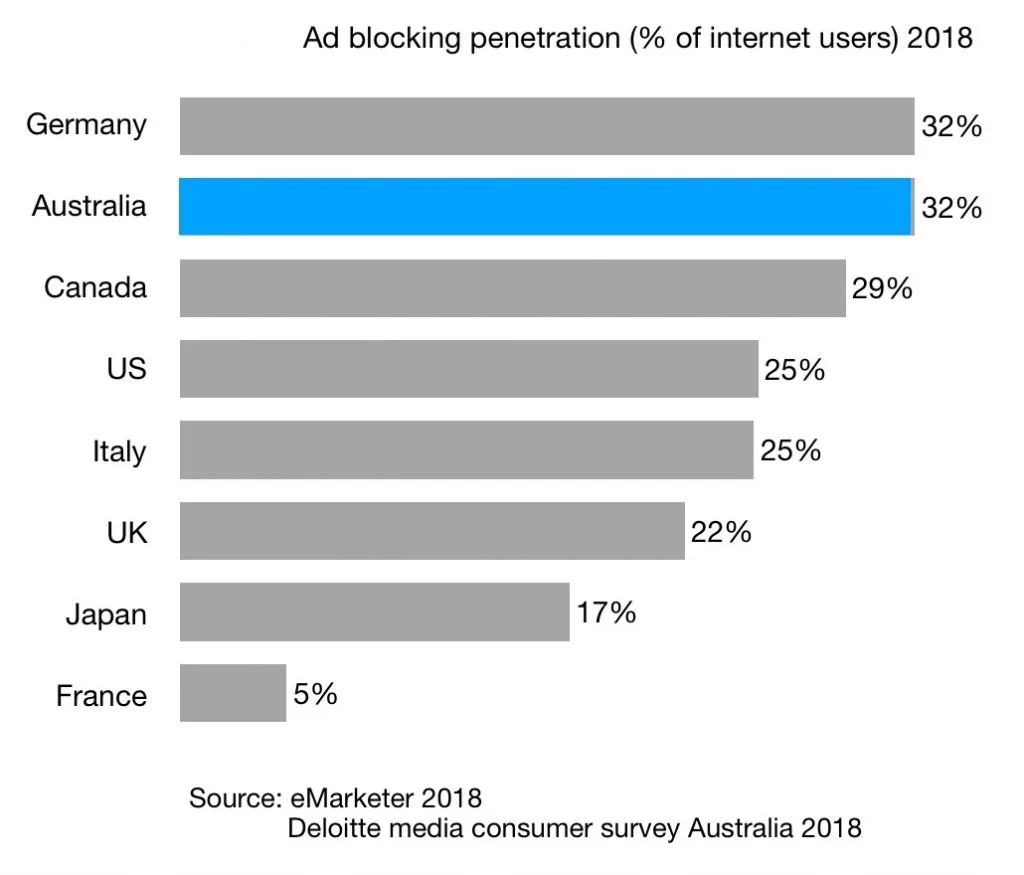

8. Ad blocking penetration in Australia is the highest in comparison to other G7 countries

From the same Deloitte report, the Australian ad blocking penetration rose from 28% in 2016 to 32% in 2018. This increase is similar to the UK.

That's all from me for today.

Cheers,

Chandler