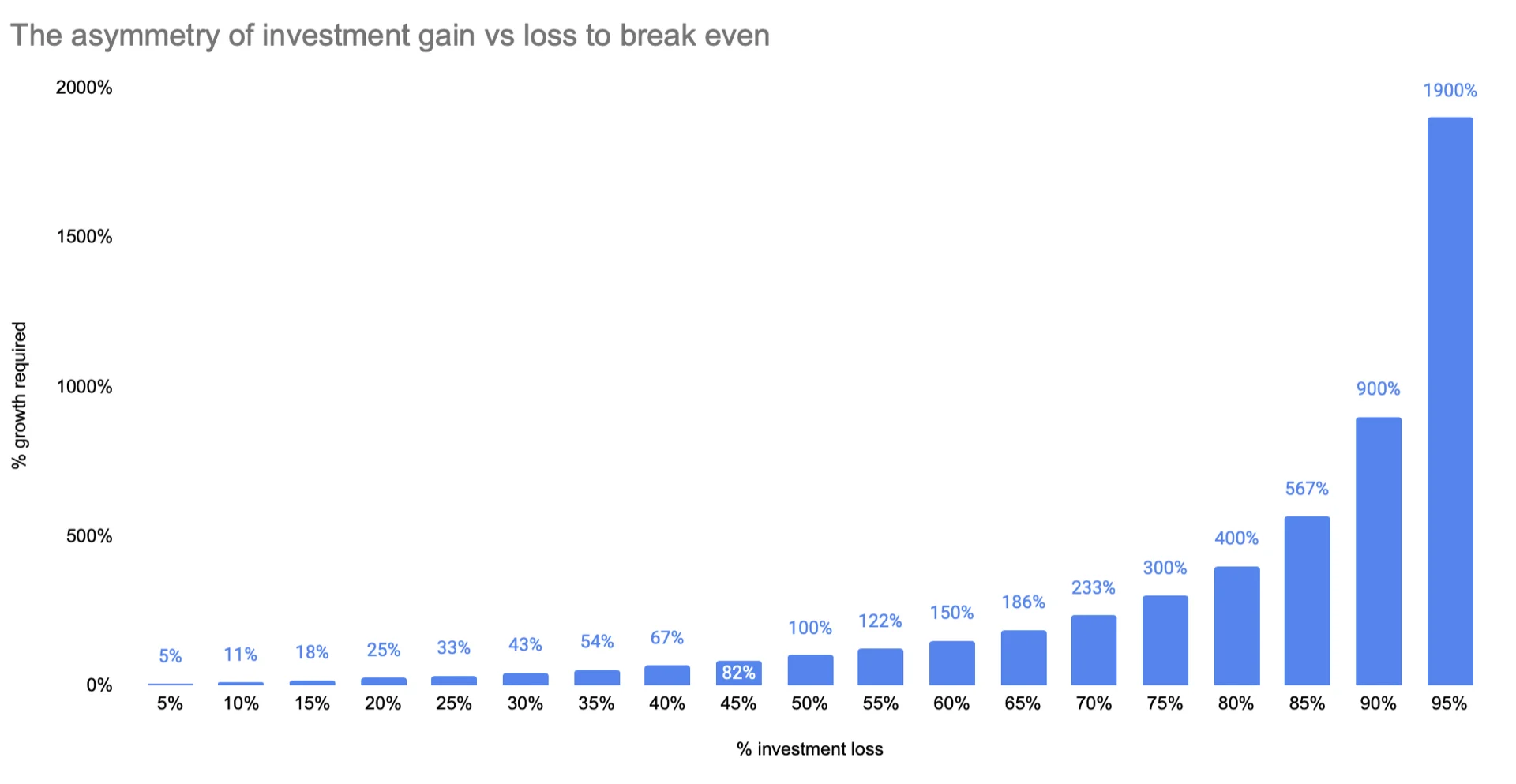

The asymmetry of investment gain vs loss to break even

A 25% investment loss doesn't require a 25% gain to break even—you actually need 33%. This mathematical asymmetry means losses hurt far more than equivalent gains help.

I learned this lesson the hard way. When I first started investing after moving to the US, I assumed gains and losses were symmetrical — lose 25%, gain 25%, you're back to where you started. Simple math, right? Nope. Not even close.

If your investment loses 25% of its value, you actually need a 33% gain just to break even. That gap widens dramatically the bigger your loss gets, and I have to admit, the math shook me when I first worked it out.

Look at the graph above. Lose 50% of your investment? You need to double your remaining money — a 100% gain — just to get back to zero. That's not a typo. You need to 2X your money to break even.

And if you lose 95%? You need to 19X your money. At that point you're basically hoping for a miracle T.T

Why This Matters (Especially for Expats)

Coming from Singapore, where I mostly had CPF and conservative savings, the US investment landscape felt like a different planet. In Asia — at least in my family and social circle — the default was to save conservatively. Fixed deposits, property, maybe some blue-chip stocks. The idea of putting a large portion of your money into the stock market felt risky, almost reckless. Then I moved to the US and discovered that here, not being in the market is considered the risky move. Colleagues talked about their 401(k) allocations and index fund strategies the way my friends in Singapore talked about property prices. The cultural pressure to be aggressive with investments is real, and for someone who grew up with Asian savings habits, it can feel like whiplash.

I think that cultural shift is broadly good — conservative savings alone will not keep up with US inflation and cost of living — but understanding this asymmetry changed how I think about risk. It is a useful counterweight to the "just put it all in the market" advice you hear constantly here.

From my experience, the takeaway is simple: protecting against big losses matters more than chasing big gains. A 10% loss only needs an 11% gain to recover — manageable. A 50% loss needs 100% — that could take years. The math is brutally unforgiving as losses get larger.

What I actually do with this knowledge

I am still very much a student when it comes to investing (I might be wrong about plenty of things), but this asymmetry is why I lean heavily toward broad index funds like VTI or VXUS rather than picking individual stocks. An index fund can drop, sure — but it is almost impossible for it to go to zero, which means you stay in the "recoverable loss" zone on that chart above. Individual stocks can and do lose 80-90%, at which point the math becomes nearly impossible. This concept of loss asymmetry is one I keep coming back to whenever I am tempted to take on more risk than I should :P

Has this asymmetry ever bitten you? I'd love to hear how others think about managing downside risk.

Cheers,

Chandler