The Expat's Guide to Understanding and Improving Your FICO Score in the US

As an expat, I learned that a good FICO score can save you thousands in interest—but understanding the multiple versions and calculation factors is key to building credit fast.

Updated for 2026: This post was originally published in 2022. For the latest strategies and a comprehensive guide, see Building Credit in the US as an Expat: The Complete 2026 Guide.

I'm going to be honest: when I moved from Singapore to the US, I had no idea what a FICO score was. In Singapore, there's a credit bureau, sure, but it doesn't dominate your financial life the way FICO does here. Within my first few weeks, I realized this three-digit number would affect everything — my ability to rent an apartment, get a credit card, even the interest rate on a future car loan. Starting from zero was humbling, to say the least T.T

If you're unfamiliar with the FICO score, it's the most widely used credit score in the US, with more than 90% of top lenders relying on it. Fair Isaac Corporation created it about 30 years ago. This post is my attempt to distill what I think is most important to know, especially from an expat perspective. I might be wrong on some nuances — I'm still learning this stuff myself — but this is what's helped me.

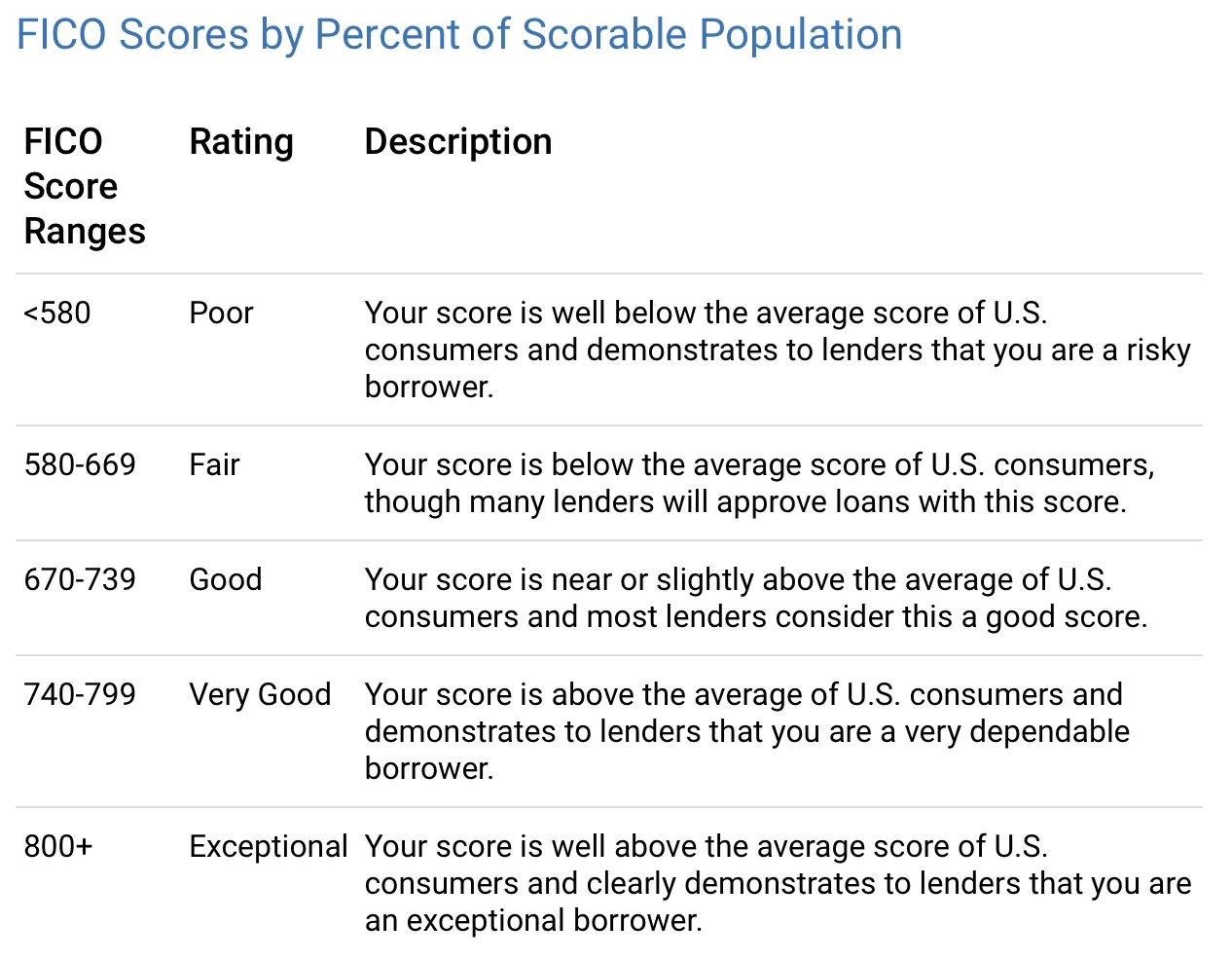

What is a FICO score?

FICO Scores are a three-digit number based on the information in your credit reports. They help lenders decide who to lend money to and at what rate. Different lenders have different ideas of what counts as "good," but here's the rough breakdown:

A good FICO Score can save you literally thousands of dollars in interest and fees. And while FICO is the most widely used, it's not the only credit score out there — other models calculate things differently.

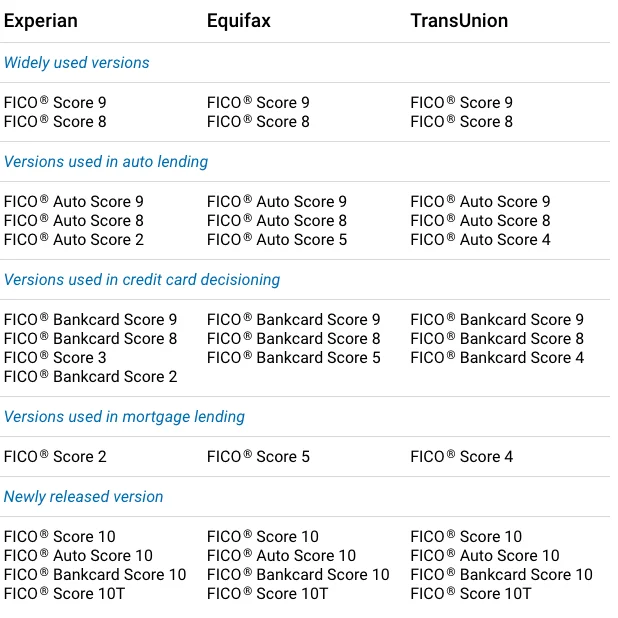

There are different FICO score versions

This part confused me at first. There isn't just one FICO score — there are multiple versions :P

"As consumer demand for credit, consumer use of credit, lender credit-granting requirements, and data reporting practices evolve over time, we periodically redevelop the FICO Score model to provide a more predictive score to lenders and consumers." (from the FICO website). FICO Score 8 and 9 are the most widely used versions right now, with FICO Score 10 being the latest. Some lenders take a while to upgrade, so you might see different scores depending on where you check.

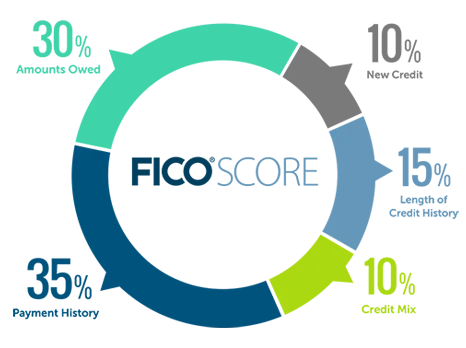

How is the FICO score calculated?

Here's the overview:

Five categories, each weighted differently. Let me walk through what I've learned about each one.

Payment history (35%) — the big one

This is the single most important factor, and honestly, it makes sense. Lenders want to know: have you been paying your bills on time?

"Payment history shows how you've paid your accounts over the length of your credit. This evidence of repayment is the primary reason why payment history makes up 35% of your score... your track record of payment tends to be the strongest predictor of the likelihood that you'll pay all debts as agreed to." (from the FICO website)

This covers credit cards, retail accounts, installment loans, mortgages — all of it. The good news is that a few late payments won't destroy you. "An overall good credit history can outweigh one or two instances of late credit card payments." But having no late payments doesn't guarantee a perfect score either.

The really serious stuff — bankruptcies, lawsuits, wage attachments — those can stay on your report for 7-10 years. So, you know, avoid those :)

Amount of debt (30%) — watch your utilization

This is the second-biggest factor. It's not just about how much you owe, but your credit utilization ratio — how much of your available credit you're actually using. If your total credit limit across all cards is $10,000 and you have $3,000 in outstanding balances, that's a 30% utilization rate.

From my experience, keeping utilization low is one of the fastest ways to improve your score. Having debt doesn't automatically make you a high-risk borrower, but maxing out your cards does raise red flags.

One trick I learned: paying off your card in full each month doesn't necessarily show as $0 on your credit report. The balance that shows up is whatever you owe on your statement closing date. So if you know when your statement closes, you can pay down the balance before that date to keep the reported number low. This small timing trick genuinely helped me.

Length of credit history (15%)

The good news for expats: even without a long credit history, you can still have a decent FICO Score if everything else looks solid. But it helps to start early.

A practical tip: don't close your oldest credit account. Closing it shortens your average credit history length, which can hurt your score. I learned this one from a fellow expat who made that mistake. Keep that first card open, even if you barely use it.

Credit mix (10%)

This refers to the variety of credit types you have — credit cards, installment loans, retail accounts, etc. It's only 10% of your score, so I wouldn't go opening random accounts just for diversity. But over time, having a healthy mix does help.

One thing to be careful about: applying for multiple new credit lines within a short period can lower your score, because lenders may see it as a sign of financial distress.

New credit (10%)

Every hard inquiry (when a lender checks your credit for a new application) temporarily dings your score by a few points. The system does allow for "rate shopping" — if you're comparing mortgage rates, for example, multiple inquiries in a short window count as one.

Checking your own credit report? That's a soft inquiry and doesn't affect your score at all. So check away. And once you have your credit established, I strongly recommend freezing your credit reports to protect the score you have worked hard to build.

And here's a silver lining: a new credit card with a large credit limit can actually help by reducing your overall utilization rate.

That's the FICO crash course from one expat to another. If you want to dig deeper, I also wrote about how to apply for a credit card without impacting your credit score.

What's been your experience building credit as an expat? Any tips I missed? I'd genuinely love to learn from your experience too.

Cheers,

Chandler

P.S. You can join Asian Expats in the US on Facebook to share and discuss more tips directly.