The Pros and Cons of Choosing a High Deductible Health Plan (HDHP): A Guide for Expats in the US

HDHPs offer lower premiums and HSA tax advantages, but require careful consideration of your health needs and financial situation to determine if the upfront costs outweigh long-term savings.

Updated for 2026: This post was originally published in 2023. For the latest IRS figures and a comprehensive guide, see Expat Healthcare Benefits in the US: HSA, FSA & HDHP Guide (2026).

During my first open enrollment in the US, I stared at the health plan options my employer sent over and genuinely did not understand the difference between half of them. Back in Singapore, healthcare was relatively straightforward — CPF Medisave, some employer coverage, done. Here in the US, I was suddenly expected to choose between PPOs, HDHPs, HMOs, and a bunch of other acronyms that nobody explains to you unless you ask.

I eventually chose an HDHP, and I want to share my reasoning along with the pros and cons — because I think this is one of those decisions where there is no universally right answer. It really depends on your situation.

(Before we start — as with any financial decision, please do your own research carefully to make an informed decision. The information here is for informational purposes only and is subject to change.)

What is a High Deductible Health Plan?

According to the IRS, an HDHP has:

- "A higher annual deductible than typical health plans, and

- A maximum limit on the sum of the annual deductible and out-of-pocket medical expenses that you must pay for covered expenses. Out-of-pocket expenses include copayments and other amounts, but don't include premiums."

An HDHP may provide preventive care benefits without a deductible or with a deductible less than the minimum annual deductible.

In plain terms: you pay more out of pocket before your insurance kicks in, but your monthly premiums are lower. Once you hit the out-of-pocket maximum, your insurance covers 100% of additional covered expenses for the rest of the year.

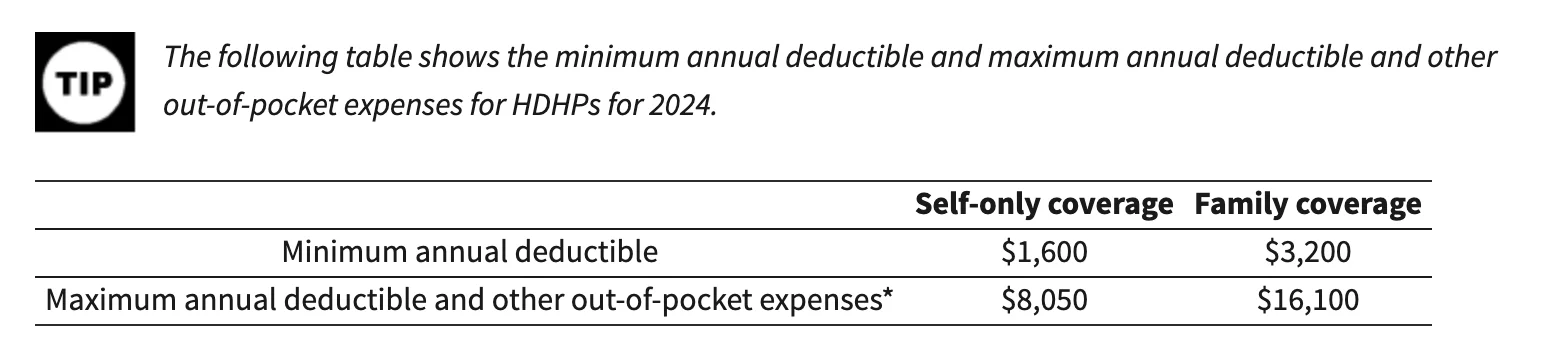

For 2024, the IRS sets these thresholds for HDHPs:

The big feature of HDHPs is that they are often paired with a Health Savings Account (HSA). An HSA is a tax-advantaged savings account for qualified medical expenses — deductibles, copays, prescriptions. Contributions are tax-deductible, the funds grow tax-free, and withdrawals for medical expenses are tax-free. It is basically triple tax-advantaged, which I think is one of the better financial tools available in the US.

The pros (why I went with an HDHP)

Lower monthly premiums and HSA tax benefits

The lower premiums were the initial draw for me. When I compared the monthly costs side by side, the HDHP saved us a meaningful amount each month. Paired with HSA contributions, the tax savings added up.

For example, if you contribute $5,000 per year to your HSA and your top marginal tax rate is 24%, you save $1,200 on taxes. That is real money you would have spent on healthcare anyway — you are just doing it more efficiently.

It encourages you to be more proactive about health

I have to admit, having a high deductible made me more conscious about preventive care. Because if something does go wrong, it costs a lot out of pocket T.T. Many HDHPs cover preventive services at no cost — annual check-ups, cancer screenings, vaccinations, wellness programs.

From the IRS, preventive care includes:

- Periodic health evaluations, including tests and diagnostic procedures ordered in connection with routine examinations

- Routine prenatal and well-child care

- Child and adult immunizations

- Tobacco cessation programs

- Obesity weight-loss programs

- Screening services (cancer, heart disease, infectious diseases, mental health, and more)

It motivates you to shop around

Here is something I did not expect: having an HDHP pushed me to actually compare prices between different healthcare providers. And the price differences are staggering — I am talking 5x to 10x for the same service with comparable quality. I am not kidding.

If you want your jaw to drop, read "The Price We Pay" by Marty Makary, MD. It is a New York Times bestseller about predatory pricing in US healthcare, and it changed how I approach medical expenses.

The cons (what to watch out for)

Higher out-of-pocket costs when something goes wrong

This is the obvious downside. If you or a family member has a chronic condition or an unexpected medical event, you are paying a lot more before insurance kicks in. For families with ongoing medical needs, this can be a serious financial burden.

You might avoid care because of the cost

I have noticed this tendency in myself — there were times when I hesitated to go to the doctor for something minor because I knew the full cost would come out of my pocket. This is not a good habit, and I actively work against it, but the temptation is real.

Shopping around takes time and energy

Yes, comparing healthcare prices can save you money. But it also takes time — time you could spend on work, family, or anything else. From my experience, the research burden is real, especially when you are new to the US and still learning how the healthcare system works.

How to decide if an HDHP is right for you

Your health situation

If your family is generally healthy and you do not anticipate frequent medical visits, an HDHP can make a lot of financial sense. If you have chronic conditions or anticipate significant medical expenses (a pregnancy, for example), a traditional plan with lower deductibles might be worth the higher premiums.

Your anticipated expenses

Run the numbers. Look at what you spent on healthcare last year (or estimate based on your family's needs) and compare the total cost under each plan option — premiums, deductibles, copays, everything.

HSA availability and employer contributions

Check if the HDHP your employer offers is HSA-eligible and whether your employer contributes to your HSA. Some employers add money to your HSA as an incentive, which can help offset the higher deductible.

Provider network

Make sure your preferred doctors are in the plan's network. I learned this one the hard way — I assumed our pediatrician was covered, and had to double-check before enrollment closed.

Employer incentives

Some employers offer additional incentives for choosing an HDHP — wellness program discounts, HSA matching, and similar benefits. Ask your HR team about what is available.

This list is not meant to be exhaustive. Healthcare is deeply personal, and I am definitely not a qualified advisor on this topic — just an expat who had to figure it out from scratch :)

My take

For our family, the HDHP made sense because we are generally healthy, the HSA tax benefits are significant, and the lower premiums freed up cash for other expenses (like Sophie's activities and saving for the future). But I recognize this would not be the right choice for everyone.

If you are going through open enrollment right now and feeling overwhelmed — I get it. Take the time to compare your options carefully, and do not be afraid to ask your HR team questions. They have seen it all before.

What has your experience been with HDHPs? Did you go with one, or did you choose a different plan type? I would love to hear how other expats are navigating this.

Cheers,

Chandler

P.S. I recently created a group on Facebook called Asian Expats in the US so that we can share and discuss more tips directly. Feel free to join.