揀High Deductible Health Plan (HDHP) 嘅Pros同Cons:美國Expats指南

HDHPs offer lower premiums同HSA tax advantages,但需要careful consider你嘅health needs同financial situation去determine upfront costs係唔係outweigh long-term savings。

2026年更新: 呢篇文章最初喺2023年publish。如果想睇最新IRS數字同comprehensive guide,請參考 Expat Healthcare Benefits in the US: HSA, FSA & HDHP Guide (2026)。

喺我第一次美國open enrollment期間,我望住employer send嚟嘅health plan options genuinely唔明白一半。喺新加坡,healthcare相對straightforward——CPF Medisave、一啲employer coverage,搞掂。喺美國,我突然被expect喺PPOs、HDHPs、HMOs同一大堆冇人explain嘅acronyms之間揀。

我最後揀咗HDHP,我想share我嘅reasoning同pros and cons——因為我覺得呢個係一個冇universally right answer嘅decisions。Really depends on你嘅situation。

(開始之前——同所有financial decisions一樣,please do your own research carefully make informed decision。呢度嘅information只係for informational purposes同subject to change。)

咩係High Deductible Health Plan?

根據IRS,HDHP有:

- "比typical health plans更高嘅annual deductible,同

- Annual deductible同你must pay for covered expenses嘅out-of-pocket medical expenses sum嘅maximum limit。Out-of-pocket expenses包括copayments同其他amounts,但唔包括premiums。"

HDHP可以provide preventive care benefits without deductible或with deductible less than minimum annual deductible。

用簡單嘅話講:你喺insurance kick in之前要pay更多out of pocket,但monthly premiums更低。一旦你hit out-of-pocket maximum,你嘅insurance cover餘下嘅covered expenses 100% for the rest of the year。

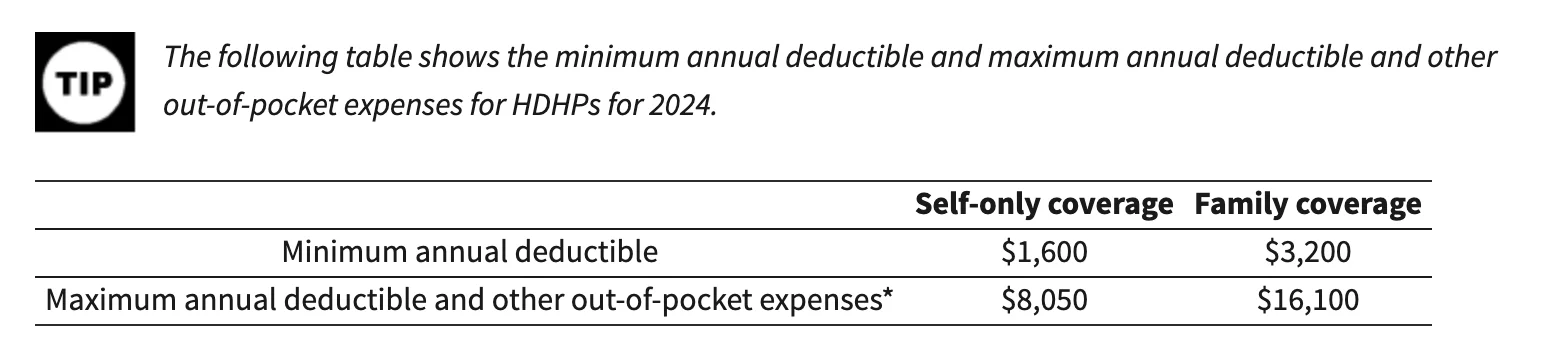

For 2024,IRS set咗HDHPs嘅呢啲thresholds:

HDHPs嘅big feature係佢哋通常paired with Health Savings Account (HSA)。HSA係一個tax-advantaged savings account for qualified medical expenses——deductibles、copays、prescriptions。Contributions係tax-deductible,funds grow tax-free,同withdrawals for medical expenses係tax-free。基本上係triple tax-advantaged,我覺得係美國available嘅better financial tools之一。

Pros(點解我揀咗HDHP)

Lower monthly premiums同HSA tax benefits

Lower premiums係initial draw for me。當我side by side compare monthly costs,HDHP save咗我哋每個月meaningful amount。Paired with HSA contributions,tax savings add up。

例如,如果你每年contribute $5,000到HSA同你嘅top marginal tax rate係24%,你save $1,200 on taxes。呢個係real money你本來都會spend喺healthcare——你只係更efficiently咁做。

佢encourage你更proactive咁對待health

我要承認,有high deductible令我更conscious about preventive care。因為如果有嘢出事,out of pocket好貴 T.T。好多HDHPs cover preventive services at no cost——annual check-ups、cancer screenings、vaccinations、wellness programs。

由IRS,preventive care包括:

- Periodic health evaluations,包括routine examinations嘅tests同diagnostic procedures

- Routine prenatal同well-child care

- Child同adult immunizations

- Tobacco cessation programs

- Obesity weight-loss programs

- Screening services(cancer、heart disease、infectious diseases、mental health同更多)

佢motivate你shop around

呢個係我冇expect嘅:有HDHP push咗我actually compare唔同healthcare providers嘅prices。而price differences係staggering——我講緊同一個service comparable quality但5x到10x嘅差距。我唔係開玩笑。

如果你想jaw drop,讀"The Price We Pay" by Marty Makary, MD。呢本係New York Times bestseller關於美國healthcare嘅predatory pricing,佢改變咗我approach medical expenses嘅方式。

Cons(要注意嘅嘢)

出事嘅時候higher out-of-pocket costs

呢個係obvious downside。如果你或family member有chronic condition或unexpected medical event,insurance kick in之前你要pay好多。對有ongoing medical needs嘅families,呢個可以係serious financial burden。

你可能因為cost而avoid care

我notice到自己有呢個tendency——有幾次我hesitate去睇doctor for minor嘢因為知道full cost會由my pocket出。呢個唔係good habit,我actively work against佢,但temptation係real。

Shopping around要時間同energy

Yes,compare healthcare prices可以save錢。但亦要時間——你可以spend喺work、family或其他嘢嘅時間。由我experience,research burden係real,尤其當你new to美國仲learning healthcare system點運作。

點decide HDHP啱唔啱你

你嘅health situation

如果你嘅family generally healthy同唔anticipate frequent medical visits,HDHP可以make好多financial sense。如果你有chronic conditions或anticipate significant medical expenses(例如pregnancy),traditional plan with lower deductibles可能worth higher premiums。

你嘅anticipated expenses

Run the numbers。睇吓你last year spend咗幾多喺healthcare(或estimate based on family needs)同compare每個plan option嘅total cost——premiums、deductibles、copays、everything。

HSA availability同employer contributions

Check你employer offer嘅HDHP係唔係HSA-eligible同employer有冇contribute to你嘅HSA。有啲employers add money到你HSA作為incentive,可以幫offset higher deductible。

Provider network

確保你preferred doctors喺plan嘅network入面。我the hard way learn咗呢個——我assume咗我哋嘅pediatrician covered,要喺enrollment close之前double-check。

Employer incentives

有啲employers offer additional incentives for choosing HDHP——wellness program discounts、HSA matching同similar benefits。問你嘅HR team有咩available。

呢個list唔meant to be exhaustive。Healthcare好personal,我definitely唔係qualified advisor on this topic——只係一個要由scratch figure out嘅expat :)

我嘅Take

For我哋家庭,HDHP make sense因為我哋generally healthy,HSA tax benefits significant,同lower premiums free up cash for其他expenses(好似Sophie嘅activities同saving for the future)。但我recognize呢個唔係適合everyone嘅choice。

如果你而家going through open enrollment感覺overwhelmed——I get it。Take time carefully compare你嘅options,同唔好afraid問HR team questions。佢哋seen it all before。

你嘅HDHP experience係點?你揀咗HDHP定另一個plan type?我好想聽其他expats點navigate呢個。

祝好,

Chandler

P.S. 我最近喺Facebook開咗一個group叫做 Asian Expats in the US,歡迎加入。