Health saving accounts (HSA) - For expats in the US: what you need to know

HSAs offer expats triple tax advantages—deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses—making them essential for savvy healthcare planning.

Updated for 2026: This post was originally published in 2022. For the latest IRS figures and a comprehensive guide, see Expat Healthcare Benefits in the US: HSA, FSA & HDHP Guide (2026).

When I first moved to the US from Singapore, the healthcare system was easily the most confusing part of settling in. In Singapore, you walk into a clinic, see a doctor, and pay a reasonable amount — simple. Here, I was suddenly dealing with deductibles, copays, coinsurance, out-of-pocket maximums, and a whole alphabet soup of plan types. I felt completely lost.

Then someone at work mentioned "HSA" and I nodded along like I knew what that meant. I did not :P

After doing my own research, I realized HSA is actually one of the best financial tools available in the US — especially for expats who are used to a simpler healthcare system and want to make the most of what is available here. Let me share what I have learned.

(Please note that this is based on my own experience and research as an expat. Rules change, so please do your own research before making financial decisions. And if you prefer to listen instead of reading, you can turn the below content into podcast using DIALØGUE.)

So what is an HSA, really?

A Health Savings Account is a special savings account that lets you set aside money — before taxes — to pay for medical expenses. Think of it as a personal healthcare piggy bank, except the government gives you tax breaks for using it.

The catch: you need to be enrolled in a High-Deductible Health Plan (HDHP) to qualify. For 2023, that means your health plan has an annual deductible of at least $1,500 for individuals or $3,000 for families, according to the IRS.

If you are not sure whether your employer offers an HDHP, check with your HR or Benefits team. I also wrote about the pros and cons of choosing an HDHP if you are weighing your options.

Why I think every eligible expat should consider it

Here is the part that blew my mind: HSA has a triple tax advantage. I am not a tax expert, but from what I understand, this is one of the only financial tools in the US that gives you all three:

- Tax-deductible contributions — the money you put in reduces your taxable income. If your top marginal tax rate is 24% and you contribute $5,000 to HSA, you save $1,200 on taxes. That is real money.

- Tax-free growth — any investment gains inside the HSA are not taxed. No capital gains tax. Coming from Singapore where there is no capital gains tax anyway, this felt familiar :D

- Tax-free withdrawals — as long as you use the money for qualified medical expenses, you pay no tax when you take it out.

I genuinely did not believe this was real when I first read about it. I kept thinking, "There must be a catch." There are some limitations (I will get to those), but the core benefit is as good as it sounds.

How it works in practice

After you sign up and start contributing, your HSA provider will send you a debit card linked to your account. When you have a qualifying medical expense, you use that card. Simple.

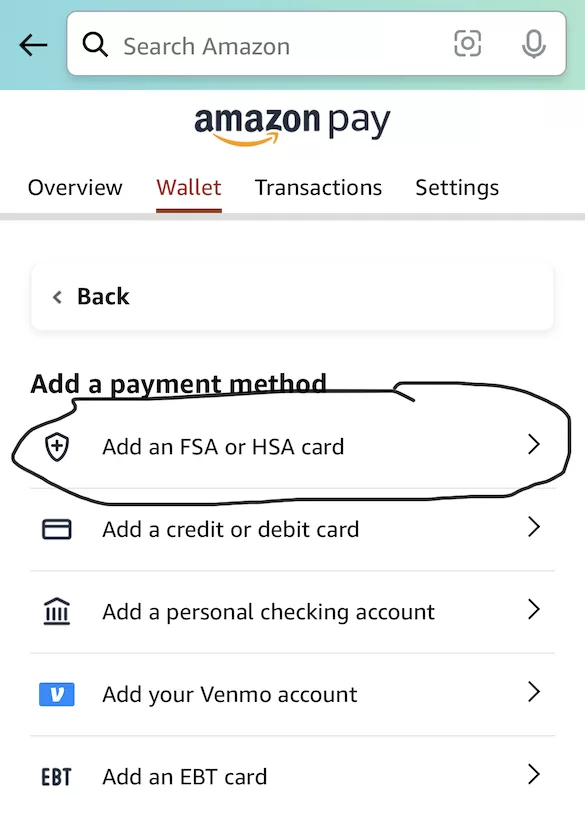

Here is a practical tip I wish someone had told me earlier: you can add your HSA debit card to Amazon under "Add an FSA or HSA card." When you shop, Amazon flags items that are HSA-eligible, and you can pay directly with the card. That was a nice surprise.

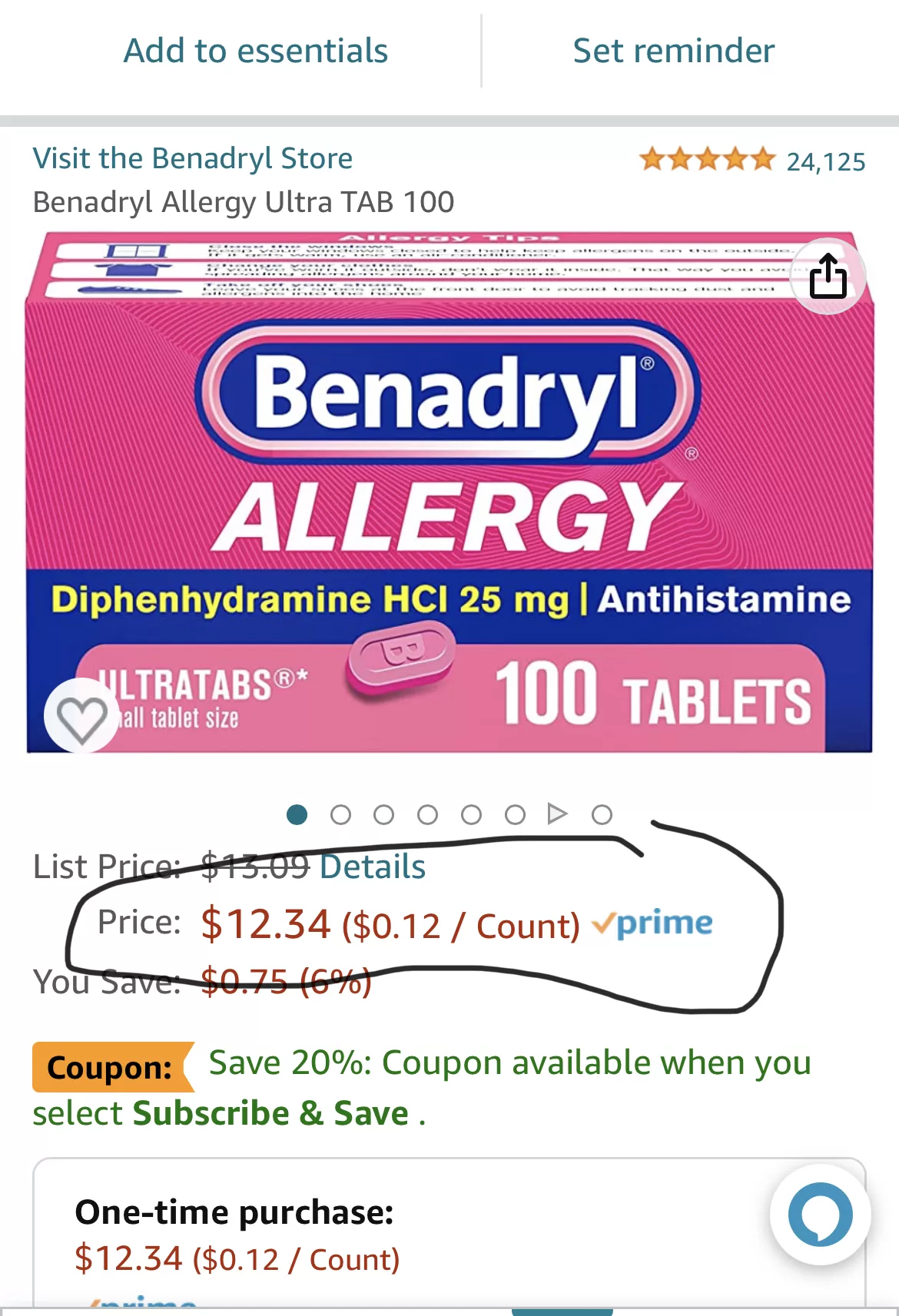

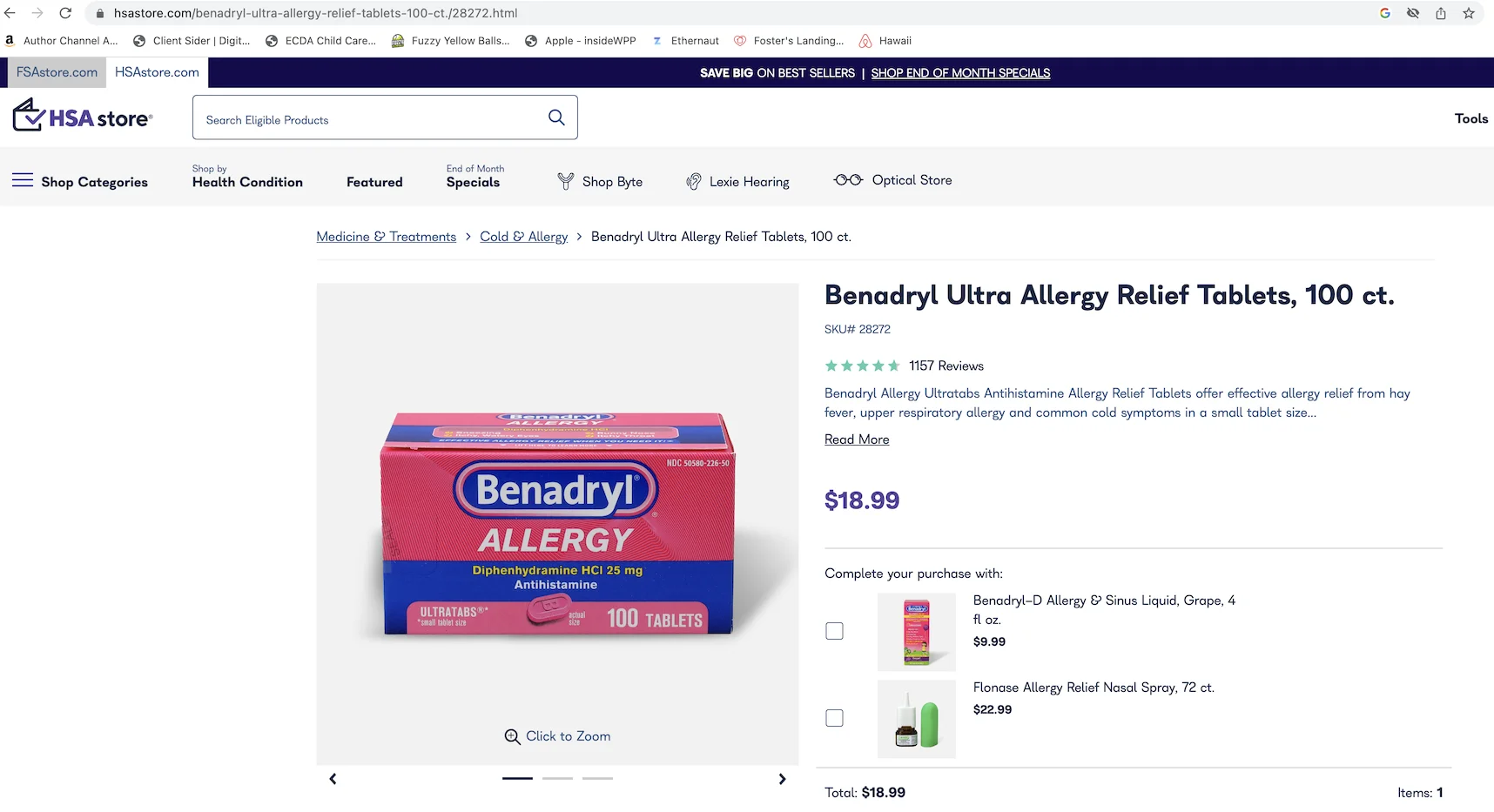

One thing to watch out for: do not just buy from the HSA Store without comparing prices. I found that Benadryl was 50% more expensive on HSA Store compared to Amazon — and you can use your HSA card on Amazon too. The same with Advil. Always compare.

How much can you contribute?

The IRS sets annual limits. For 2023, it was $3,850 for individuals or $7,750 for families. For 2024, it went up to $4,150 for individuals or $8,300 for families. If you are 55 or older, you can contribute an additional $1,000.

My approach: I max it out every year. The tax savings alone make it worthwhile, and the money rolls over — unlike an FSA, there is no "use it or lose it" rule. Whatever you do not spend stays in your account and keeps growing.

The limitations (because nothing is perfect)

I would be dishonest if I did not mention the downsides:

- You need an HDHP. That higher deductible means you pay more out-of-pocket before insurance kicks in. For a family that visits the doctor frequently, this can be a real consideration.

- Contribution limits exist. If you have very high medical expenses, the HSA alone may not cover everything.

- Non-medical withdrawals get penalized. If you take money out for non-medical reasons before age 65, you pay income tax plus a 20% penalty. After 65, it is just income tax — which makes it work like a traditional retirement account.

- You generally cannot have both FSA and HSA. However, if your employer allows it, you may be able to contribute to a limited-purpose FSA (LPFSA) alongside your HSA.

Despite these limitations, I think the benefits far outweigh the drawbacks for most expats with eligible plans.

A few things people always ask me

Does my HSA stay with me if I change jobs? Yes. Your HSA is portable — it is yours regardless of where you work. This was a relief for me to learn.

Can I open an HSA on my own? Yes, after you enroll in an HSA-eligible HDHP. You do not need to go through your employer.

What happens if I never spend the money? It rolls over indefinitely. No expiration. This is one of the biggest differences from FSA, and honestly the reason I prefer HSA.

Who are the major HSA providers? According to Morningstar, the four largest in 2022 were HealthEquity, Optum, Fidelity, and HSA Bank. You can also check what tools like Optum's expense eligibility checker to see what qualifies as a medical expense.

The bottom line

I think HSA is one of those things that sounds complicated at first but is actually quite straightforward once you understand it. The triple tax advantage is genuinely hard to beat :D I might be wrong, but I believe every expat with an eligible plan should at least consider it.

Are you an expat using HSA? Or thinking about it? I would love to hear about your experience. Did you find any tricks that I missed?

Cheers,

Chandler

P.S: George Kamel made a video about HSA that is informative and entertaining. You can check it out below.

https://www.youtube.com/watch?v=nasI\_NQHOrA

P.P.S: I created a group on Facebook called Asian Expats in the US so that we can share and discuss tips directly. Feel free to join.